A recent study published by researchers from the London Business School found that retail traders brought into the market by last year’s Gamestop Rebellion saga fueled by the WallStreetBets subreddit of social marketing and influencing platform Reddit lost more than US$5 billiion during the stock market’s bull run.

Analyzing trading data that became available after a 2019 regulatory change, the 87-page paper, published on April 20 in SSRN, states retail traders lost an astonishing $1.14 billion on directly failed trades between November of 2019 to present.

But more notably, researchers discovered that the same group lost several multiples more in fees paid to market makers, which amounted to an additional $4.13 billion in aggregate trading costs.

The performance of retail traders was directly inverse to the overall market, “For the same period, all options trades returned a gain of $5.48 billion,” the article states.

OPRA and SLAN

LSB revealed they were able to ascertain concrete statistics on the performance of retail traders by utilizing a reporting requirement imposed by the Options Price Reporting Authority (OPRA) targeting trades coded as SLAN, which according to an OPRA document available online, stands for Single Leg Auction Non-ISO.

Success

You are now signed up for our newsletter

Success

Check your email to complete sign up

The document describes SLAN-coded trades as being “traded in a two sided auction mechanism that goes through an exposure period,” often referred to as a price improvement auction.

These trades — considered to be primarily executed by amateur traders — were measured by volume and defined as “SLAN Share” in the study.

Researchers also focused on options trades composed of small sizes in the range of 10 contracts or less, which are frequently — and more commonly — utilized by cash-restricted ordinary people trading on the side.

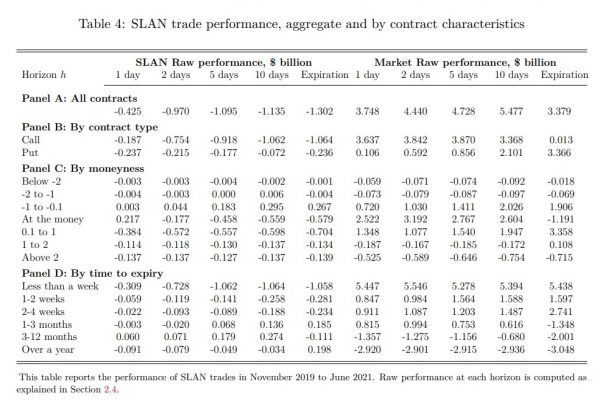

The team discovered that the dollar volume of SLAN-coded trades had increased by 143 percent while the same figure for small position trades had increased by 224 percent from November of 2019 to present.

WallStreetBets, Robinhood, and Gamestop

LSB researchers definitely found that both SLAN Share and net SLAN-coded purchases were “positively correlated with stock-based measures of retail activity, such as ticker mentions on WallStreetBets forum and Robinhood ownership breadth.”

GAMESTOP REBELLION FALLACY

- Big Media Puts ‘Gamestop Rebellion’ on Par with Capitol Riots

- Wall Street Behemoths Ate Reddit’s Gamestop Lunch

- Amateur Investors Fodder, Not Driver of GameStop’s Meteoric NYSE Climb

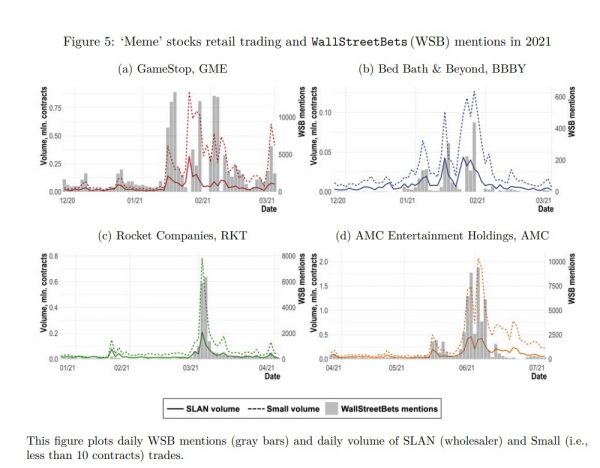

Specifically, the team found a remarkable correlation when plotting SLAN volume and small trading volume against mentions on r/WallStreetBets for meme stocks Gamestop (GME), Bed Bath & Beyond (BBBY), Rocket Companies (RKT), and AMC Entertainment Holdings (AMC).

The price of all four securities enjoyed significant increases correlated to heavily promoted phases on r/WallStreetBets.

Bagholding AMC

In the case of AMC, data shows that while the movie theater had long since been largely unnoticed on Reddit, it first received a sudden bout of mentions, approximately 2,000 per day, in the later part of May of 2021.

As AMC’s mentions rose, trading volume for small contract positions correspondingly increased from close to zero to 500,000 contracts.

As this occurred, AMC’s stock price had already enjoyed significant gains, going from a close of $10.32 on May 12, 2021 to a high of $14.67 only a few trading days later on May 18.

While data showed that WSB mentions and small contract trades primarily died down after the initial May 18 bump, by June 1, AMC had already tripled, opening at $31.89.

STOCK MARKET SHARK TANK

- Robinhood Alternative Webull Hides its China Roots

- Ex-Lehman Bros Trader Charged in Alleged Multi-billion Dollar Viacom, Discovery Pump Scheme

- Silver Bullion Supply Scarce, Premiums High Amid Wall Street Stockpiling

- Twitter Stock Rises Over $16 Billion 40 Days After Banning Trump

Noise was quiet until the middle of the month, when the WallStreetBets marketing platform began to lure retail traders back into the market.

However, by that time, AMC had again doubled, trading at a high of $64.71 on June 15.

During the month of June, as WSB mentions reached as high as 7,500 each day, AMC opened at $31.89, posted a high of $72.62, and closed at $56.68.

Everything changed in July, however, when the stock cratered, posting a low of $31.15 before closing at $37.02.

AMC has been on a ceaseless downward slide ever since, closing the week of April 25 at $15.30, a 78.9 percent loss off the June of 2021 high.

More volume, more fees

Researchers focused on the controversial way in which “zero commission” gamified trading apps such as Robinhood and other brokerages generate their revenue, called Payment for Order Flow (PFOF).

The practice first gained public prominence during a February of 2021 House Committee on Financial Services inquiry on the Gamestop Rebellion debacle where Robinhood CEO Vladimir Tenev was forced to concede his company was on the verge of liquidation.

During the meeting, Rep. Brad Sherman (D-CA) pushed the issue to the surface when he pressured Tenev and market maker Citadel Securities CEO Kenneth Griffin about how “zero commission” platforms stay in business.

Sherman said there are “two ways to pay the folks involved in Wall Street for buying and selling a stock.” The first, he said, was commission.

The Rep succinctly described PFOF when he stated, “The other way to do it is to give them [retail traders] a worse execution.”

A simple way to understand PFOF is that users of apps such as Robinhood are not executing their buys and sells on open exchanges such as the Toronto Stock Exchange or the New York Stock Exchange.

Instead, Robinhood routes the transactions through “dark pool” market makers, such as Griffin’s Citadel, and is paid fees for the liquidity provided in the process.

The result for the consumer is that they’re still paying commission, it’s just that fees are hidden in the difference between the buy or sell price executed compared to the buy or sell price on exchanges.

The LSB study stated, “The brokerage therefore has an incentive to encourage investors to trade more and to trade assets with larger spreads, which could be to their detriment.”

Researchers also noted that the advent of the options market had made the PFOF scheme considerably more lucrative for wholesalers such as Robinhood, “In the second quarter of 2021, brokerages in the U.S. received more than 284.4 million dollars of PFOF for their order flow in stocks and 581.2 million dollars for options.”

Specifically, the $4.13 billion LSB researchers say retail traders lost in trading fees alone “are not as transparent as brokerage fees, and are likely to be overlooked by retail investors,” noting they “become revenue for market makers and exchanges executing retail orders.”

They estimated that the $4.13 billion was composed of only $773 million in direct commission charged to traders.

The remainder is what amateur traders paid in various contractual fees composed by the exceptional bid-ask spreads and downsides of small trading sizes.

Gambling, not investing

In the paper’s Conclusion, researchers determined “retail investors enter the options market for speculative reasons.”

Additionally in the study’s preamble, the team stated that newcomers “also have preferences for lotteries and opt for ultra short-term (weekly) options…participate in trading frenzies, and incur large trading costs (possibly masked by zero-commission offers).”

They also found that based on trading size, frequency, and the remarkable bid-ask spread — averaging an astonishing 23.4 percent — “that retail investors are entering the options market with an intent to speculate rather than hedge.”

Overall, the paper described newcomers to the market as “mainly young and tech-savvy, yet inexperienced investors.”

Losing habits

The team found some bad habits of losing newcomers to the options market.

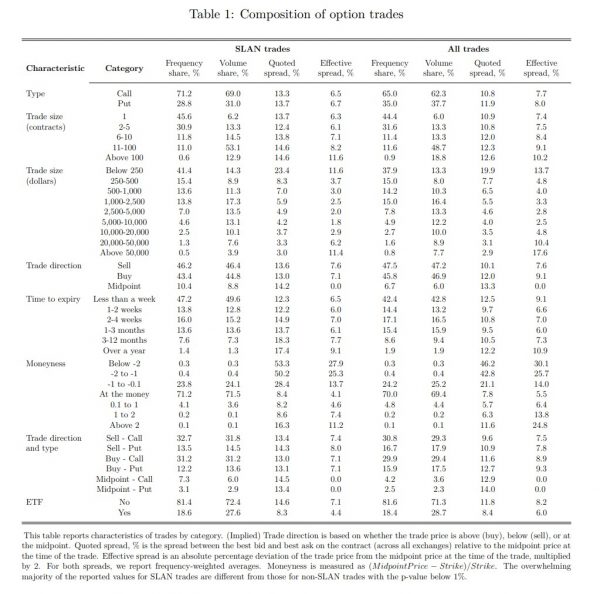

Specifically, 69 percent of purchased contracts were calls (option to buy), rather than puts (option to sell), meaning traders were tunnel visioned on attempting to profit from the rise of a security and would not profit during corrections.

72 percent of contracts were purchased at-the-money, which the team noticed suffered a bid-ask spread that averaged a painful 28 percent.

An additional 24 percent of contracts purchased were slightly out-of-the-money.

Furthermore, more than 41 percent of all trades were a position size of under $250, which incurred a bid-ask spread of 23.4 percent.