By Trevor Hunnicutt, Alun John and Rae Wee, Reuters

Bank stocks around the world plunged on Monday even as President Joe Biden vowed to take whatever action was needed to ensure the safety of the U.S. banking system after the sudden collapse of Silicon Valley Bank and Signature Bank.

Biden’s efforts to reassure markets and depositors came after emergency U.S. measures to shore up banks by giving them access to additional funding failed to dispel investor worries about potential contagion to other lenders worldwide.

The White House said the Treasury Department is working with regulators on the next steps.

With investors fearing additional failures, major U.S. banks lost around $90 billion in stock market value on Monday, bringing their loss over the past three trading sessions to nearly $190 billion.

Success

You are now signed up for our newsletter

Success

Check your email to complete sign up

Shares of First Republic Bank tumbled as news of fresh financing failed to reassure investors, and so did Western Alliance Bancorp and PacWest Bancorp.

First Republic had been able to meet withdrawal demands on Monday with the help of extra funding from JPMorgan Chase, the mid-cap lender’s executive chair, Jim Herbert, told CNBC, adding it was not seeing a massive deposit outflow.

Shock waves extended to Europe, where the STOXX banking index closed 5.7% lower. Germany’s Commerzbank fell 12.7%, while Credit Suisse slid 9.6% to a new record low.

Swiss financial regulator FINMA said it was closely monitoring banks and insurers, while a senior European Central Bank supervisor said the board overseeing the euro zone’s biggest banks did not see any need for an emergency meeting.

Biden said his administration’s actions over the weekend meant “Americans can have confidence that the banking system is safe,” while also promising stiffer regulation after the biggest U.S. bank failure since the 2008 financial crisis.

“Your deposits will be there when you need them,” he said.

Nevertheless, shares of big U.S. banks, including JPMorgan Chase & Co, Citigroup, and Wells Fargo all lost ground on Monday.

An administration official said there was no timeline for Biden to make any requests of Congress as his aides were still working to manage the immediate situation and better understand it.

In the money markets, indicators of credit risk in the U.S. and euro zone banking systems edged up.

“When a step (is taken) this big, this quickly, your first thought is ‘crisis averted.’ But your second thought is, how big was that crisis, how big were the risks that this step had to be taken?” said Rick Meckler, partner at Cherry Lane Investments.

Emboldened by bets that the U.S. Federal Reserve may have to slow its rate hikes, and with investors seeking safe havens, the price of gold raced above the key $1,900 level.

“There is a sense of contagion and where we see a repricing around financials is leading to a repricing across markets,” said Mark Dowding, chief investment officer at BlueBay Asset Management in London.

U.S. regulators stepped in on Sunday after the collapse of SVB, which had a run after a big bond portfolio hit.

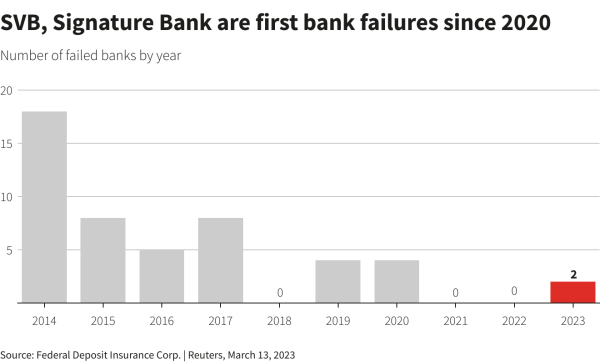

GRAPHIC – SVB, Signature Bank are first bank failures since 2020 SVB, Signature Bank are first bank failures since 2020

SVB Financial Group and two top executives were sued on Monday by shareholders, who accused them of concealing how rising interest rates would leave its Silicon Valley Bank unit “particularly susceptible” to a bank run.

SVB’s customers will have access to all their deposits from Monday and regulators set up a new facility to give banks access to emergency funds and the Fed made it easier for banks to borrow from it in emergencies.

Regulators also moved swiftly to close New York’s Signature Bank, which had come under pressure in recent days.

“A serious investigation needs to be undertaken on why the regulators missed red flags … and what needs to be overhauled,” said Mark Sobel, a former senior Treasury official and U.S. chair of think tank OMFIF.

Fallout

Companies around the globe with SVB accounts rushed to assess the impact on their finances. In Germany, the central bank convened its crisis team to assess any fallout.

After marathon weekend talks, HSBC said it was buying the British arm of SVB for one pound ($1.21).

While SVB UK is small, its sudden demise prompted calls for government help for Britain’s startup industry, and its heavily exposed biotech sector in particular.

Prime Minister Rishi Sunak added his voice to those in the UK saying there was no concern about systemic risk.

“Our banks are well capitalised, the liquidity is strong,” Sunak told ITV during a visit to the United States.

A furious race to reprice interest rate expectations also sent waves through markets as investors bet the Fed will be reluctant to hike next week.

The Fed’s options are limited, said Sobel. “The Fed could cut rates, but that has its own drawbacks. So the Fed and Treasury have kind of shot their bazooka for now. I think it’s a question of the market steadying out. Is this a one-off adjustment in regional banks, or does it portend more to come?”

Traders currently see a 50% chance of no rate hike at that meeting, with rate cuts priced in for the second half of the year. Early last week a 25 basis-point hike was fully priced in, with a 70% chance seen of 50 basis points.

The yield on the U.S. two-year Treasury note briefly fell below 4% for the first time since last October and was last down 53.1 basis points (bps) at 4.057%. The two-year note’s yield, which reflects interest rate move expectations, was on track for the biggest one-day drop since October 1987.

On Monday morning, U.S. bank regulators sought to reassure nervous customers who lined up outside SVB’s Santa Clara, California, headquarters, offering coffee and donuts. “Feel free to transact business as usual. We just ask for a little bit of time because of the volume,” FDIC employee Luis Mayorga told waiting customers.

The first customer, who did not want to be named, said they arrived at SVB at 4 a.m.